Top 10 Reasons Not to Lease a Car

Leasing a car might seem like a cool way to drive something new every few years, but it’s not always the best deal for everyone. There are a few hidden downsides that can cost you more in the long run. Let’s dive into 10 reasons not to lease a car and why it might make more sense to look at other options like buying a car instead.

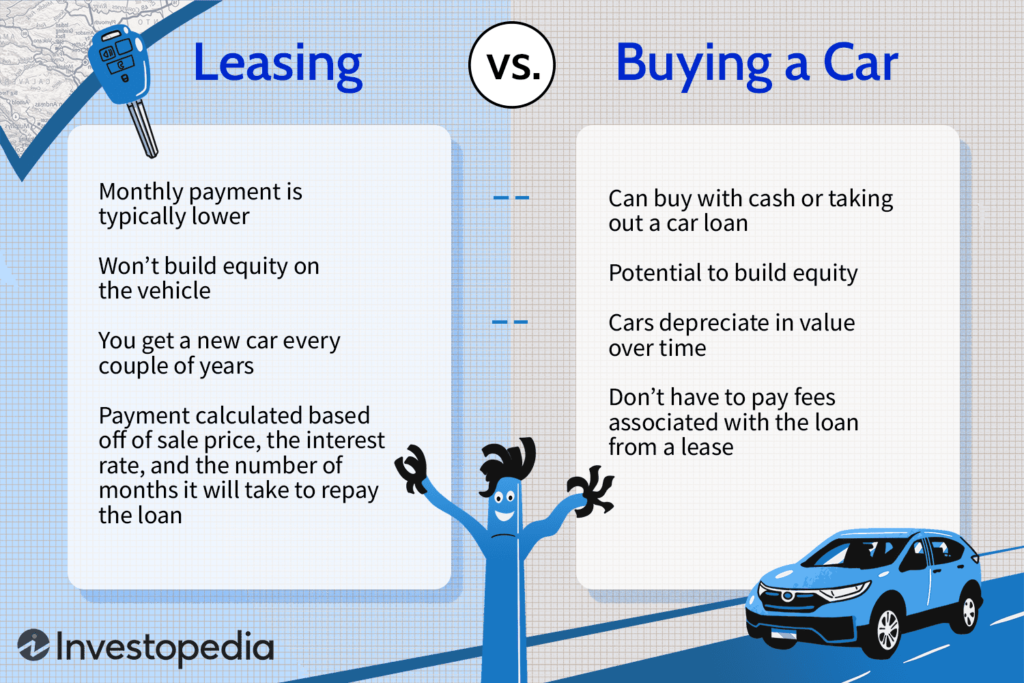

1. You Don’t Own the Car

When you lease a car, you’re basically renting it. At the end of the lease term, you don’t get to keep it. Unlike buying, where you eventually own the car outright after your payments, leasing leaves you with nothing but the experience of driving a new car for a while.

2. Mileage Limits Can Be a Hassle

Leased vehicles often come with mileage restrictions, like 10,000 to 12,000 miles a year. Go over that limit, and you’ll have to pay a fee for every extra mile. If you have a long commute or love road trips, leasing can end up costing you way more than you expect.

3. Higher Insurance Premiums

Leased cars usually require higher insurance coverage because the leasing company wants to protect their investment. This means you’ll be paying more for insurance than you would if you owned the car outright. Over time, this adds up and makes leasing more expensive.

4. Early Termination Is Expensive

If you decide to end your lease agreement early, you’re in for a big bill. Leasing contracts have strict rules, and breaking them often means paying hefty penalties. Whether your needs change or the car isn’t working out, you don’t have the same flexibility you’d have with a car loan.

5. No Customization Allowed

Leased vehicles must be returned in the same condition you got them, aside from normal wear and tear. Want to add a cool spoiler or update the sound system? Forget it. Leasing contracts don’t allow any major changes, so you’re stuck with the car exactly as it is.

6. You’re on the Hook for Repairs

While new cars often come with a warranty, you’re still responsible for certain maintenance costs. Plus, if there’s excessive wear and tear on the car—like scratches, dents, or stains—you’ll have to pay for it. These costs can pile up, making leasing less appealing.

7. No Equity Means No Value

When you lease, your payments only cover the car’s depreciation and some leasing fees. Unlike buying, where you’re building equity in the car over time, leasing leaves you with nothing to show for your money once the lease term ends.

8. Leasing Can Cost More in the Long Run

Lease deals might look affordable upfront, but over time, the cost of leasing can add up. Since you’ll always have a lease payment, you’ll end up spending more in the long run compared to owning a car outright. Plus, if you keep leasing new cars, those costs never stop.

9. Penalties for Excessive Wear and Tear

Normal wear is okay, but excessive wear and tear, like worn-out tires or damage to the interior, can cost you when you return the car. Leasing companies are picky about how the car looks and functions, so you’ll likely have to pay for repairs before handing it back.

10. What Happens If the Car Is Totaled?

If your leased car is totaled in an accident, your insurance might not cover the entire lease payment you still owe. This gap can leave you stuck with a big bill, even though you don’t have the car anymore. Gap insurance can help, but it’s an extra cost you’ll need to consider.

Is Leasing Right for You?

While leasing on the other hand can work for some people, like those who drive less or love getting a new car every few years, it’s not for everyone. The mileage limits, lack of ownership, and higher interest rates can make it a poor financial choice for many. If you’re thinking about leasing, weigh these 10 reasons not to lease a car carefully before signing a lease agreement.

If you’d rather save money in the long run, buying a car might be a smarter move. Owning your car means you can drive as much as you want, customize it, and eventually enjoy years without car payments.

Also Read This: How Many Miles Is Good for a Used Car?